Cha Ching: Online Banking and Investing

The rise of neobanks, whitespace for Chime, and the newest investing platforms

Here’s an interesting thought experiment. Imagine you’re trying to build the next decacorn or hectocorn - a startup whose valuation exceeds $10Bn or $100Bn. You might want to know what startups of that flavor typically look like - are there any trends around geography or industry? We know there are two current private hectocorns - SpaceX and Bytedance. SpaceX commands a $100Bn valuation and ships over 10 commercial space flights per year for cumulatively north of $1Bn. Bytedance is a media juggernaut that encompasses TikTok (which we all know), but also a portfolio of other media apps such as Helo (an Indian app), Douyin (Chinese TT), and Huoshan (a short-form video app). To no surprise these are companies that cater to a large swath of users - there is nothing niche about these services (except for perhaps SpaceX serving a wealthy niche) - the goal of both is to revolutionize travel and media consumption for the masses. We expect a similar feature (broad-based, revolutionary) to carry over with the most valuable decacorns.

Which decacorns do we focus on? According to the latest 2021 data from CBInsights, the top 10 decacorns by valuation span $25Bn - $95Bn. This is a huge range, considering the next ten are valued between $14Bn and $25Bn, a much narrower band. Most of the latter group are in Asia. So in order to learn from the most successful stand-outs globally (East and West), let’s focus on the first batch of ten for this article:

What jumps out is that most of these decacorns (six) are consumer fintech companies, tech companies with a B2C model improving money exchange, management, and deployment for everyday consumers. Some of this makes sense ex post facto. Consumer fintech targets activities that are recurrent, ubiquitous, and vital to livelihoods. I’m referring to things like digital payments, consumer and SMB lending, and investment management companies (broadly defined) like Robinhood and Betterment. Digital payments are ubiquitous: global non-cash transactions hit 709Bn transactions in 2019. Cash transactions were just 30% of all payments in the U.S. in 2017. Digital lending platforms are projected to grow from $10.7Bn in 2021 to nearly double that in 2026, which reflects a double digit growth rate. Consumers from all walks of life are always seeking out the best rates when taking out home, auto, and small business loans. Opening an online bank account via Revolut, Nubank, or Chime (all on the list above) is a step in the right direction. Finally, Robinhood has $80Bn in assets across 18 million accounts and just IPO’d last year. Again, fintech is ubiquitous.

In this article, we carve a slice from the consumer fintech universe and focus on:

How digital banks drive interchange fees

How stock trading startups differentiate themselves

Companies in these areas have been immensely successful (just look at the list above) and I’m itching to figure out why.

I. How digital banks drive interchange fees

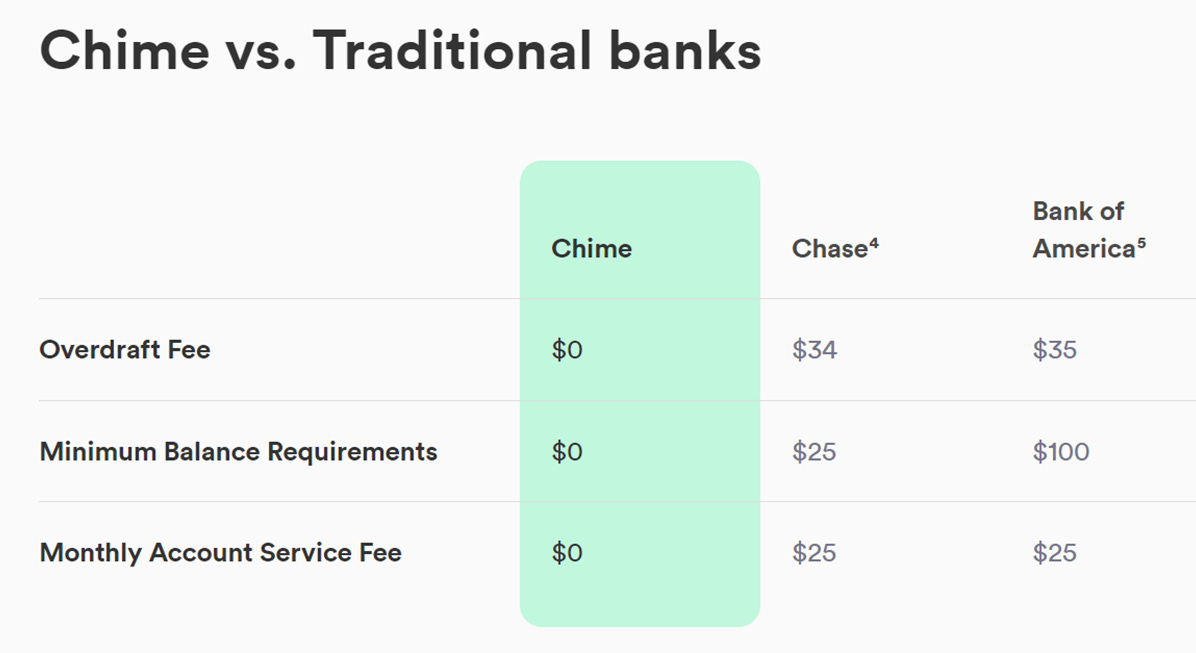

For the longest time, we’ve gone to Bank of America, Wells Fargo, and JP Morgan Chase for our banking needs. Traditional banks like these allow you to store money and make payments, and they collect various fees in exchange. However, these fees are onerous. There are overdraft fees incurred for spending profligately, minimum balance requirements, and account service fees. Rex Woodbury, a columnist I enjoy following at Index Ventures, has written about the various ways in which traditional banking has failed us - how the average borrower takes 20 years to pay off a loan, and how the average overdraft fee has ballooned from 1998 to 2018. JP Morgan Chase makes $2Bn from overdraft fees per year.

As a response, over the past few years, we’ve seen the rise of neobanks, or online only banking. Though you can’t visit a neobank’s branch, they are slick, easy, and offer a compelling value proposition vs. the traditional player - no fees. Consider Chime from our decacorn list above - Chime’s a neobank that doesn’t charge overdraft fees or require a minimum balance (see above). Between Chime and its neobank peers, consumers are gravitating increasingly to a paperless form of banking. This migration towards neobanks will likely continue; consider the projected growth below, via eMarketer data as of May 2021. We’ll have about 56 million neobank account holders by 2025, many newly minted college grads.

Chime is far and away the leading neobank in the U.S. - with 13 million users (the next largest peer is Current with 4 million). Smaller alternatives are Aspiration and Varo. Chime makes money on interchange fees - when a merchant receives a payment, a portion (~1.5%) goes to Visa; Chime takes a % of this. Through its no-fee approach, Chime attracts consumers for whom overdraft is a problem - i.e. low income households. Visually, Chime presents site visitors with snapshots of its payment interface, which looks exactly like Venmo - communicating a nice easy, familiar mode of payment. Unlike Venmo, Chime doesn’t require both parties to have a Chime account. Moreover, you can withdraw from Chime via designated ATMs at 7/11s.

Also the elephant in the room - Venmo, acquired by PayPal, is a juggernaut. It has 76 million users, not 13. It’s rolling out features like Venmo credit cards and crypto trading. A stock-trading app is on the way. According to a BofA analyst, Venmo could balloon to 120 million users by 2023. By reviewing Venmo’s growth strategies - credit card, stock trading platform, crypto - we might consider how a smaller player like Chime will grow in the future into a “super-app,” if it desires. Another large competitor in place, especially for SMB customers, is Square - which has a Cash App with over 40 million transacting users.

Can Chime and Varo take on these now established fintech players? I think so, but as Chime moves up-market and looks to fuel growth, the larger threat will be traditional blue chips rolling out services like Goldman’s Marcus. Let me explain. Right now, Chime caters its cheap offering to lower income individuals. However, Chime’s larger consumer offering is gratis; the idea is to solely drive activity to payment transactions (and thus interchange). For example, there are no annual fees for Chime’s Credit Builder Visa Credit card; it’s clearly following a different playbook from Venmo.

Will this strategy last? Only if trading volumes grow…Let’s look at the typically low income population Chime serves - according to Pew Research, lower income income has not grown much, and continues to account for <10% of total income. Here’s how wages have changed:

Below the median, income growth rates decelerate as you get richer. Over time, Chime’s customer base will not see any enormous change in their income but they’ll have needs like vacations, weddings, and home improvements. They will need personal loans to finance these and stock trading platforms to manage their minimal savings. Traditional banks like Goldman have rolled out Marcus, a solution that offers credit cards and personal loans to individuals. Once startups like Current hit Chime’s level, it is time to start thinking about offering personal loans as well, where the startups can start earning a second revenue stream from interest payments.

Dave, which offers small cash advances to meet the needs I enumerated above is well positioned in the market. It just went public in a $4Bn SPAC deal this past Thursday and presents as a possible Chime acquirer or JV partner. It’s solving a very real and present problem in America - after we’ve halted the rise of predatory lending practices, banks do not want to serve low income populations. Other larger startups and JV partners that could benefit from Chime’s payment data: Better Mortgage, Rocket, or Lending Tree. All can be kept within the Chime ecosystem as far as the consumer is concerned. Better is planning an IPO via SPAC for an $8Bn valuation. It is large enough to acquire a new source of sub-prime customers.

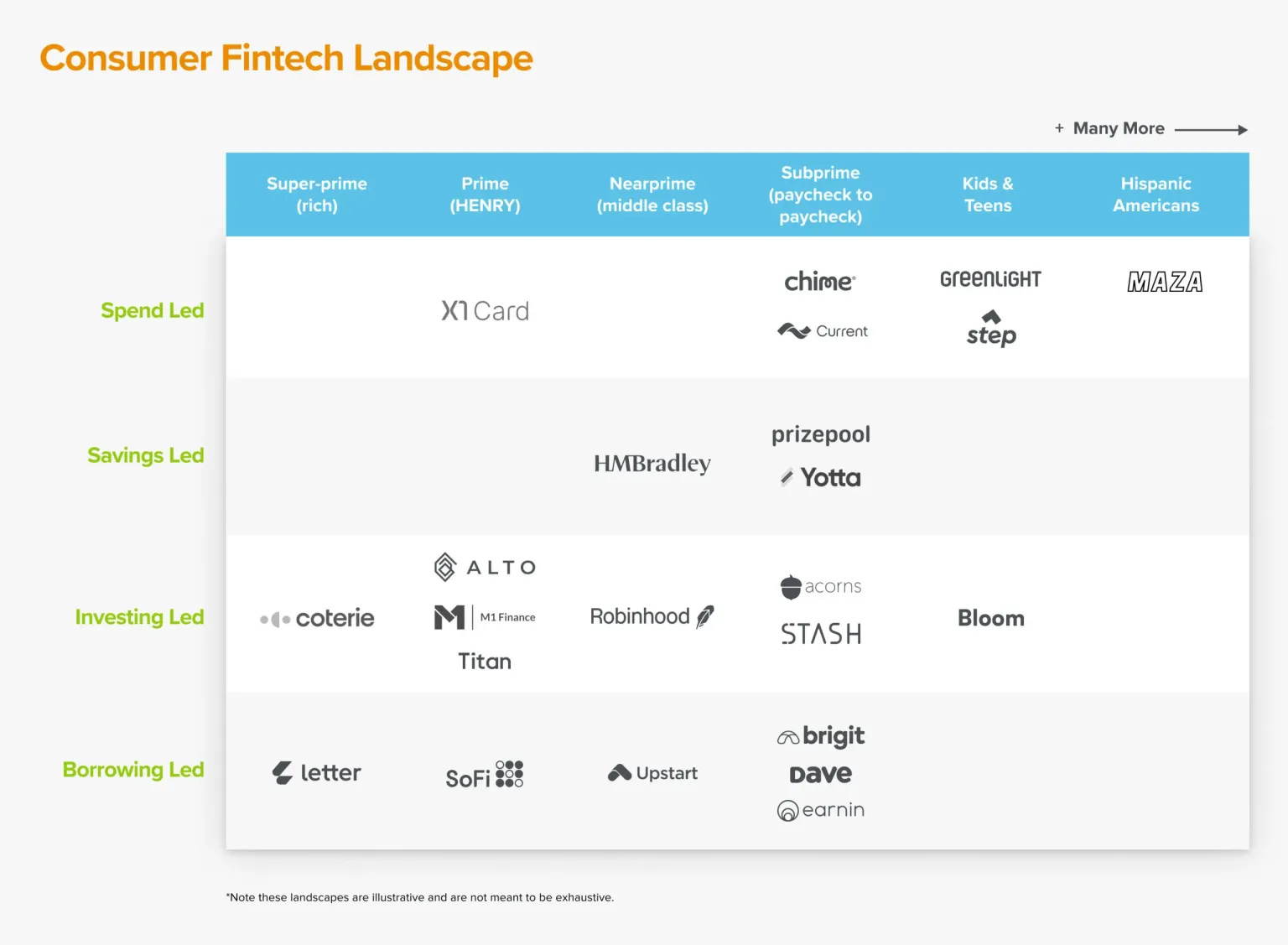

Some VCs like a16z think an assortment of fintech startups offer some combination of spending, saving, investing, and borrowing activities (see their chart I’ve pasted below). They differentiate based on which consumer segment they target- from low-credit millennials to prime HENRY’s. The only thing I’d footnote and add is that there is very much a race to become the all-service provider with a streamlined interface and no one is there yet. No-fee/Low-fee startups in the payment and lending space like Dave and Chime are best positioned to become this all purpose solution.

II. How stock trading startups differentiate themselves

One of the four pillars we talked about in the last section was investing. Let’s talk about apps that make it easier to invest your wealth - next gen stock brokerages like Robinhood. How do they differentiate themselves?

Robinhood’s transaction-based revenues in the chart below from its latest 10-Q represent 78% of its total revenue. Notice the big jump from 2020 to 2021. It’s doing well. One of the company’s biggest selling points is its no commission trading (once again, no fee), and it’s why I use Robinhood exclusively for trading despite having a legacy Etrade account. So if there are no commissions, what are these “transaction revenues”? They are basically “payment for order flow” (PFOF) in the case of equities and options trades. How this works: a Robinhood customer places an order to buy 5 shares of GOOG; they send that order to a market maker like Citadel Securities who will actually execute the trade. Citadel makes a profit for themselves off the bid-ask spread. Citadel then kicks back a portion of this profit to Robinhood as PFOF, or transaction revenue.

This PFOF mechanism matters because it creates a warped incentive structure, where Robinhood might route trades to market makers that kick back greater PFOF, potentially introducing inefficiency into the market. At least this is the contention of brokerage upstart and rival Public.com, which boasts zero PFOF, among other things (i.e. lots of educational content for less sophisticated investors, a long-term investing focus). Public believes that zero PFOF aligns incentives better. Is theirs a winning marketing claim? I’m concerned that the details of how trades settle are too granular and nitty gritty for the common public choosing a brokerage app. So I’m not currently bullish on the Public claim - until they can show, say, that stock sellers on Robinhood are consistently making less than Public sellers, while buyers are making the same amount. It will be tough for them to get a hold of this data though - Citadel isn’t throwing this sensitive information out there. If Public had it, they’d show it.

That said, Public can still succeed in the short term by capturing some of the newly rich consumer base. There’s a lot of whitespace in this market. According to 2019 Pew research, 60% of Americans still don’t have investments outside their retirement accounts. And as of 2020 Gallup data, 68% (the clear majority) of Americans aged 18-29 are not invested in the stock market at all. They will adopt investing platforms in time. It’s not just about adding customers though. It’s important to drive trading activity as well once they’re on the platform. The interesting thing about the recently public Robinhood according to its latest 10-Q, is that its ARPU (average revenue per user) steeply dropped from $101 in 2020 to $65 in 2021, despite its revenue firing on all cylinders (see the note and disaggregation above). This shows Robinhood is increasingly tapping less active users and/or user growth is outstripping the pace of trading activity. To bolster trading activity among its new users, Robinhood can learn from the educational tools that the startup Public.com is employing.

Public is not alone in offering educational material. Another app on the stock trading scene is WeBull. WeBull offers helpful analysis for amateur investors and a paper trading feature which allows you to invest fake money in stocks and see how it would’ve panned out. It’s interesting that Robinhood, the $13Bn market cap player in the space, doesn’t allow this paper trading feature – probably because it eats into revenue and users can just put on smaller trades if they’re risk averse. WeBull makes up for any lost revenue by allowing users to take short positions, which Robinhood does not yet allow for. For entrepreneurs and established players in the equity brokerage space, these are helpful lessons: offer a greater palate of features, educational tools, and low-fee/no-fee accounts.

This recipe has made the established player Interactive Brokers a leading option in its field. Interactive offers tradable foreign stocks to its user base. What I find interesting with this one is the trajectory of its customer base. Interactive Brokers started off with a full scale platform for advanced traders and garnered a reputation there for being best in class. In 2019 though, Interactive Brokers launched IKBR Lite for casual investors. This is similar to Elon Musk’s popular 2006 strategy with Tesla: start at the higher end of the market with the Roadster for sophisticated drivers, and migrate down market to the cheaper Model S. Tesla reinvested profits from Roadster sales to build affordable cars for the mass market. Interactive Brokers reinvested the brand it developed amongst knowledgeable traders to build a more user friendly version for the mass market. This is one possible route to adopt for intrapreneurial teams within established brokerages.

The brokerage universe is composed of both established players offering online tools (think Fidelity and Interactive Brokers) as well as upstarts like Public. Above are some of the more modern upstarts in the space along with notes about their potential growth strategy. Below is one such upstart’s approach to consumer investing. It likely needs a revamp.

Conclusions

When it comes to fintech activities, there’s spending, borrowing, investing, and holding these three functions up, there’s storing/saving money. American fintech startups are growing along these dimensions. However, on a day to day basis, the most important pillars are spending and borrowing. Look at how much Square Cash App revenue grew in a matter of two years; it’s now over $6Bn in revenue by targeting spending and borrowing. They’ll primarily compete on merchant partnerships and visibility, alongside no-fee promises to win over large financially divided consumer segments. The all-purpose low-cost competitor will win the day. With enough users, finely curated ads will form another large revenue stream for this winner.

In a future installment of Pins and Needles, we’ll look at Revolut and Nubank, international fintech giants providing banking services.