Unleashing the Beast: The Indian Healthcare Startup Opportunity is a Roaring Tiger

Unleashing the Beast: The Indian Healthcare Startup Opportunity is a Roaring Tiger

Why Insurtech startups have greater whitespace, ePharmacy requires risk diversification, and doctor-patient communication startups are hot in India

When I was eleven, I spent summers in India, playing cricket on the dung-laden roadside with kids my age. I’d hang out with them afterwards, when they’d tell me about their favorite cricket players (their national sport), and American movies they were catching up on. The year was 2003, so I was surprised they were raving about 1997-released Titanic. There was a delay from Hollywood release date to percolation in southern India. It’s been 20 years, so the pace of globalization has increased. However, it’s still true that it takes time for Western concepts born in the United States to migrate eastward.

How long? When it comes to healthcare and health tech startups, looks like roughly 4-6 years. Collective Health, which offers employer-based health insurance solutions in the U.S., raised $32m in Mar’15 in a Series B. By the end of 2015, it secured another $80m in funding. Assuming similar levels of dilution to today, the company was worth $300m. The company recently raised a cool $280m Series F in May’21 at a $1.5Bn valuation. Investors made 5x their money in 6 years, over a 30% IRR as the company expanded beyond California to offer health insurance coverage nationwide. Plum Benefits Pvt Ltd. in India has onboarded 600 organizations and similarly offers health insurance solutions to small businesses. It is the Collective Health counterpart, raising $15.6m in Series A funding by Tiger Global. Just as Collective Health is partnered with BCBS, Plum is partnering with insurance providers like ICICI Lombard and Star Health in India. Plum Benefits is well on its way to becoming an insurtech giant in the country - but like Titanic, its dissemination in India is lagging the U.S. by 6 years.

Take Flatiron Health, a startup that has applied a big data approach to cancer research, aggregating studies from various hospitals and academic centers. The company was founded in NY in 2012, and has raised a total of $313m to date. Niramai Health Analytix, founded in Bengaluru (Bangalore) in 2016 by Dr. Geetha Manjunath, targets breast cancer screening by employing deep learning and AI detection to non-invasive thermal scans of early stage growth. Niramai has raised just $7m so far. However, there’s enormous potential for growth: once every four minutes, a woman is diagnosed with breast cancer in India, often with poor prognosis because it’s detected too late. Because it’s been a few years, Niramai is able to leverage the latest in machine learning; more so than Flatiron in 2012. Meanwhile, more recent US-based startups like Grail are landing unicorn valuations in the cancer screening blood test category using the latest in genomic testing. It would behoove Indian startups like Niramai and their venture investors to keep a close watch on Western innovation, seeing where they can invest R&D spend (for example, genetic testing) so they can innovate more quickly.

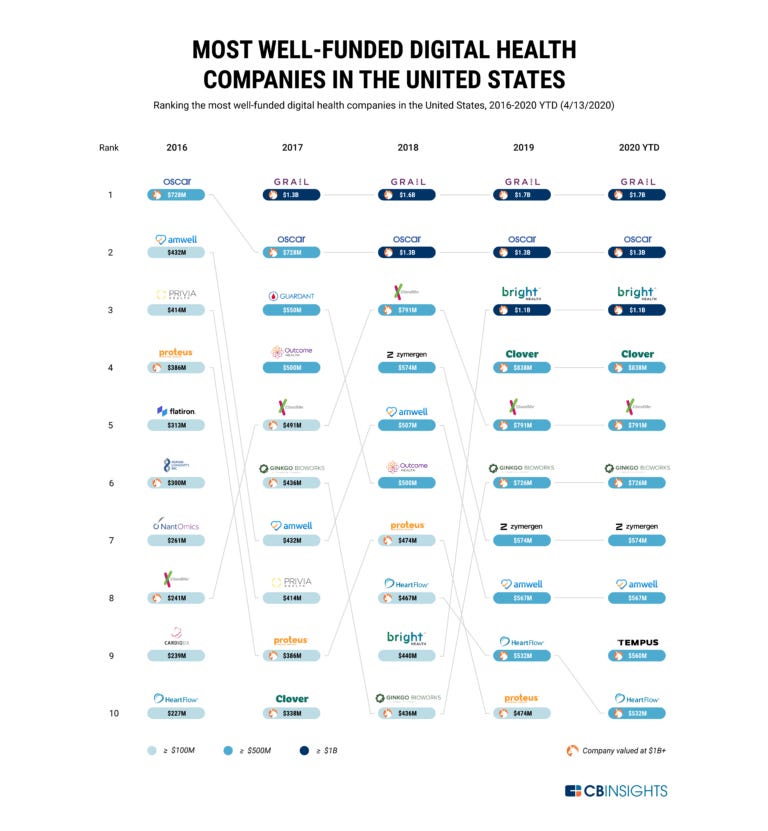

Not every healthcare startup in India is a copycat of a US-based startup. The health insurance and legislation context is different; as of April 2020, 5 of the top 10 funded health startups in the U.S. are insurance focused (see chart below). This is because employer sponsored health insurance covers 60% of the population. In India, it’s less than 1% because 80% of India is not covered by any health insurance. 70% of health expenditures in India are out of pocket (and insurance usually only covers hospitalization, not primary care), causing 50m people to fall below the poverty line. With 25% growth in private health insurance, there is tremendous whitespace for a marketplace of policy options. Policybazaar, a 12-year old startup, has been backed by SoftBank and Tiger Global and offers this kind of solution to the Indian insurance market. It has raised $630m to date. The company commands 90% of the online insurance market and is looking to expand to new geographies. Before that expansion, however, there is room to grow within the home market: namely, PolicyBazaar can start offering its own insurance product. This would be a natural way to proactively develop the Indian insurtech market.

Beyond insurance, there are three main areas where healthcare and health tech in India can benefit from investment:

AI in pharma services and drug development

EHRs and ePharmacy

Appointment booking and patient communication

Perhaps less promising are (IV) startups in India focused on the patient experience.

I. AI in Pharma Services and Medical Screening

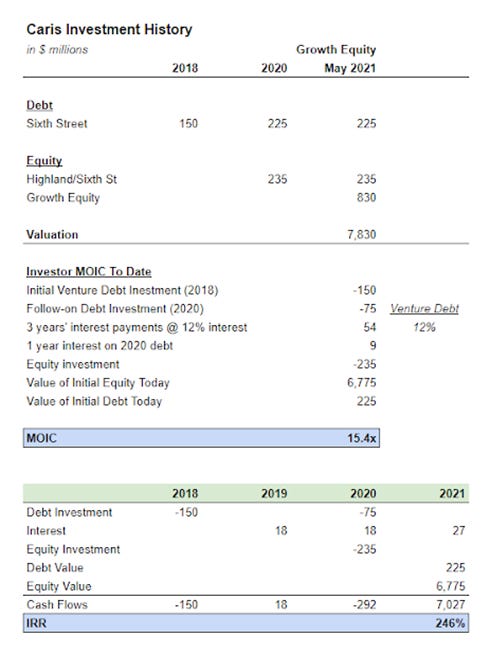

One of the largest healthcare deals in 2021 was the May’21 $830m investment by Orbimed in Caris Life Sciences, which leverages AI to target molecular biomarkers in DNA and RNA from blood tests to identify early stage cancer. This huge deal was a win for precision medicine - you can see how Sixth Street and other debt and equity investors on a whole did over the course of the investment. Now the above calculation simplifies a bit because Sixth Street led a consortium of investors in the 2020 growth capital infusion; and there’s a slightly different set of investors at different funding cycles. I’m also using a conservative venture debt assumption of 12% interest rate (sometimes, investors charge 15%). However, the 15.4x MOIC above reflects a massive expansion in investment value that you’ll see with successful investments (though VC home runs can go up to 30-50x).

We’re going to see increased personalization of medicine in India, as well. The Indian pharma services market is really not that different structurally from the U.S. For example, just as Massachusetts is a cauldron of biotech innovation, Integral Biosciences in Noida, UP, offers drug discovery services to mid-sized pharma companies and startups. When I tried to find more startups in this space, however, I came up short - suggesting that the molecular genomics and drug discovery startup field has not yet matured in India to the degree it has in the U.S. Bangalore-based Connexios, a drug discovery startup which has brokered an out-licensing deal for its diabetes formulation, is one of the first of its kind. That said, India is qualitatively different: the country, for example, is facing an overprescription-of-antibiotics crisis. Vitas Pharma is a drug discovery company targeting multi-drug resistant hospital acquired infections, a market underserved by Big Pharma apparently (I’d actually love more color here if anyone has it as to why Big Pharma is not going after these infection classes). By focusing on a problem afflicting India more acutely than developed countries, Vitas positions itself well for growth.

The real site for drug discovery innovation beyond Big Pharma would be CROs in India. A staple of healthcare private equity in the U.S. is the clinical research organization (CRO). These CROs assist Big Pharma with drug development and testing, from clinical trial enrollment to regulatory compliance. In India, CROs are also a healthcare private equity target. CX Partners, a mid-market ~600m private equity fund in India, invested in Veeda Clinical Research in 2018. As prior CX associate Vik Thakore described it to me, Veeda is a high margin business that conducts bioavailability (how the drug is reacting with the body) and bioequivalence testing (how body is reacting to the drug). Unfortunately, the company’s revenue has dropped from $29.8m to $20.3m in 2020. Meanwhile, rumblings suggest CX (the sponsor, also known as the “promoter” in India) will likely take it public in the next 12 months; but in India, 20-30% of the promoter’s holding is legally locked up for 3 years so CX cannot full exit. CX will therefore continue to be involved with the investment.

To beef up the valuation in the public markets, it makes sense for CX and Veeda to pursue AI-based detection of the appropriate drug candidates during recruitment, or machine learning applications to data generated during clinical trials. By speeding time to market, these novel applications improve Veeda’s market positioning and CX’s exit value. Private equity players in the Indian pharma services space should not discount growth capital infusions that can lift projected growth rates and valuation multiples.

II. EHRs and ePharmacy

Two areas of health electronification are (a) medical records in hospitals and clinics and (b) pharmacy delivery. These areas are at a growth inflection point in India but they’ve been noticed by large conglomerates like Tata so it will be difficult for new entrants to compete. New players willl have to target specific subsegments, like an Amazon for Ayurvedic treatment, but would benefit from publishing blog content and providing a base of relevant Ayurvedic providers (similar to what Tata is doing with 1mg), in order to derisk the venture and draw multiple sources of revenue. In this piece, I’ll focus on the second, leaving medical records for a future more global discussion.

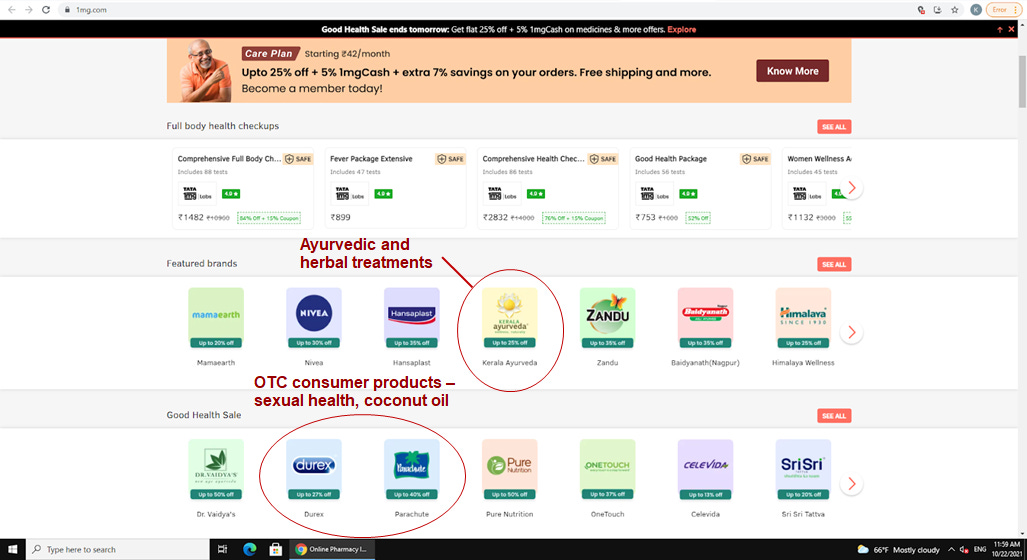

In the e-pharmacy space, Reliance has acquired Netmeds (2020) and Tata has acquired 1mg (2021). 1mg made $4.3Bn in revenue in 2020 though still saw a loss. Netmeds saw its revenue from operations fall from $2.6m to $670k in 2020, a 75% drop. There are a few takeaways from these alarming financials: (i) If e-pharmacy is going to succeed, it will likely require an unprofitable Amazon-like story first. These large marketplaces incur logistics costs for delivering medicines, but as more participants flock to the site, they’ll realize benefits of scale. The initial costs do create a moat, however, in that successful e-pharm startups will require significant initial cash funding to sustain losses, the likes of which only large corporates like Tata and Reliance or growth equity players like TPG (which backed PharmEasy, $87m revenue) can provide at scale. (ii) One way to derisk the investment is invest in adjacent segments such as e-consultations, and e-diagnostics. Tata is doing this with 1mg, investing in 3 diagnostics labs and online tele-doc consultations. Their investment has also done well financially unlike Netmeds- growing from $26.9m in 2019 to $47.7m in 2020 - possibly attributable to the Tata brand. Another de-risking strategy, which can be seen above in the NetMeds site, is the selling of Ayurvedic brands, OTC products (sexual health, oils), and 1mg private label products instead of over-indexing on OTC meds alone. Instead of Tylenol, you can see above that 1mg is selling Zandu and Iodex, brands familiar to the local population.

III. Appointment Booking and Patient Communication

Phable is an Indian startup that launched in 2018 that helps doctors prod patients to adhere to medical regimens and book follow-up appointments. At the start of this year, Phable raised a $12m round by NJ-headquartered SOSV to scale from 250k patients to 5m patients by the end of 2021. The key to Phable’s success is tapping the market participants with power - the doctors - and helping them grow revenue by 20%. This triggers wide scale adoption.

When a country with as large a population as India seeks to receive care, especially in cities, a Zocdoc type platform like Phable is immensely useful. There are other players in this space focused on improving patient-doctor communication. Lybrate raised $10.2m from Tiger Global and Ratan Tata in Jul’15 to facilitate connections between anonymous patients and doctors on the app who can provide quick advice. In as little as six months, the app grew to over 80k doctors on the platform and 100k DAUs. In recent years, the company has turned profitable (see below).

I think the main source of Lybrate’s growth will be in penetration of rural and Tier 2 cities. They’re tackling a key problem in India’s population needs. However, their physician growth has slowed in recent years (100k as of 2019). I think they’ll need to skew the service more towards telecare and providing doctors better economics, instead of the open forums where doctors receive little compensation for free advice. The fact that Phable sits on the right side of the supply-demand equation gives me more confidence in them over Lybrate. Lessons from Lybrate should inform the growth trajectory of startups that are more recently attracting funding in the same domain, such as Navia Life Care, another Indian medication adherence startup that raised $1.1m in Aug’21.

IV. Enhancing the Patient Experience for Low Income Indians

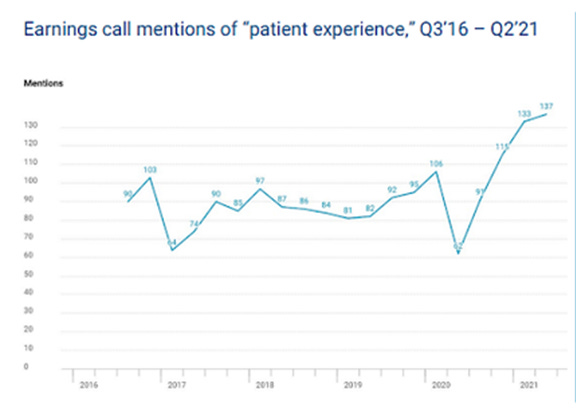

CBInsights presents the below chart to show that patient experience startups hold particular promise in the coming years as they gain corporate attention. This may hold true in the U.S. K health in NY has raised $270m to offer 27/4 doctor access for $23 visits. Circulo Health is one of various insurtech companies focused on providing Medicaid populations with better quality care.

However, this trend will not carry over well in India. I’ve received treatment in India and seen how patient care is rote and process-oriented; the same culture of patient attentiveness does not hold true - it cannot hold true given the population of nearly 1.4Bn (World Bank). According to the latest data as of 2017, the United States has 2.9 beds per 1,000 people; India 0.5. Founder of Med-Pay Ravi Chandra is quoted as saying Indian startups are more focused on ‘patient experience’ in this article, but the reality is he’s saying startups are focused on connecting patients with providers (our point earlier on Phable) - not enhancing the patient experience or quality of access for low income populations like Circulo per se. Patients in that segment need healthcare and access period - not a fancy UX or high-tech care delivery platform they can’t pay for. Pure logistics suffice.

Conclusions

Overall, I’m bullish about the state of Indian healthcare venture investment. There’s a lot of opportunity to reach the masses - through e-pharmacy and easy medical booking and private insurance schemes for the lowest income populations. There are topics I haven’t fully broached in this article, as well. For example, as Manraj Bevli, previously with Accel, tells me, Accel will probably make north of 15x on its investment in CureFit, a startup founded by ex-executives of Myntra and Flipkart that provides members with access to workout classes and gyms. As India develops and its people become more willing to spend that $50/month on trainer-led workouts and mental health sessions, CureFit will be ready to fill a need. Taking the pulse of India’s 20-35 year old demographic, a larger fraction there than it is in the U.S., through focus groups and surveys will be critical to unlocking the potential of the Indian DTC healthcare market.

Thanks to Vik Thakore and Manraj Bevli for their contributions.